3 Reasons This Brazilian Fintech Disruptor Could Be a Multibagger by 2030

Banking can be a boring sector to analyze as an investor. Not if you are following Nu Holdings (NU +0.15%), though. The digital bank that began in Brazil a little more than a decade ago has taken Latin America by storm, now counting 135 million customers.

And yet, with a market cap of $63 billion, investors are still underrating the company. Here are three reasons the Brazilian financial technology giant could be a multibagger during the next five years.

Today’s Change

(0.15%) $0.02

Current Price

$13.05

Key Data Points

Market Cap

$63B

Day’s Range

$12.89 – $13.24

52wk Range

$11.71 – $18.98

Volume

25.6K

Avg Vol

50.4M

Mexico expansion

The company’s Nu Bank unit is already dominant in Brazil, where the majority of its customers, deposits, and loans sit today. It has targeted the second-largest economy in Latin America — Mexico — as its next avenue of growth.

So far, Nu Bank is taking off like a weed in the country. Since launching in the country just a few years ago, Nu Bank now has 15 million customers in Mexico, making it the third-largest financial player in the market. It has done so through its low-fee, easy-to-use mobile banking application, bringing people modern banking products like credit cards and personal loans without the need to visit a bank branch.

Revenue in Mexico has gone from zero in 2020 to $950 million, and Nu is now breakeven on net income. There is plenty of room to keep the growth party going. Mexico’s economy is almost the same size as Brazil’s, a country that generates more than $12 billion in annual revenue for Nu Bank. Expect Mexico to keep up this impressive growth trajectory during the next five years.

Image source: Nu Holdings.

Increasing revenue per user

With more than 100 million customers, one might think Nu Bank is up against a revenue ceiling. As you can see with its early growth in Mexico, this is far from the truth.

It is also true that Nu Bank has a long runway to increase its monthly revenue per user, which hit $16 last quarter. This was up from just $3.50 in March 2020 and it still has room to grow as Nu Bank’s customer usage of credit cards, personal loans, and other banking services increases. According to management, traditional banks in Brazil earn about $40 in monthly revenue per customer, suggesting Nu Bank could more than double its revenue without adding any new customers in the years ahead.

Add in the Mexico expansion, and you can see why the company’s growth profile is so impressive.

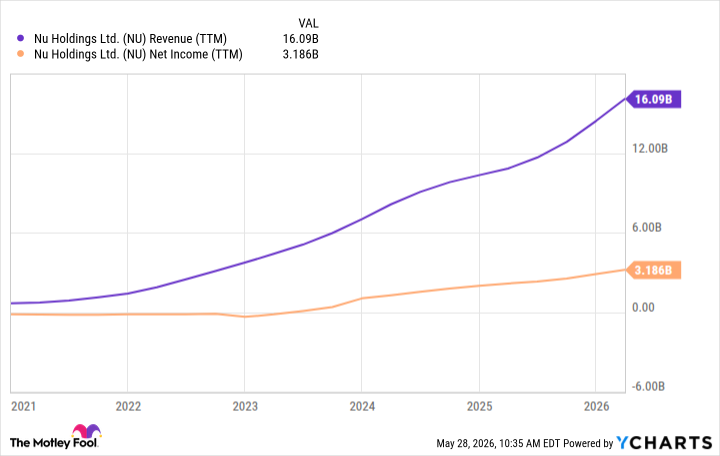

NU Revenue (TTM) data by YCharts

More operating efficiency

The trifecta for a Nu Bank investment comes from its consistent operating leverage as it expands. Its consolidated efficiency ratio — which measures overhead costs as a percentage of total revenue — fell to 18% in Q1 2026 versus 61% in Q1 2022.

This is absurd efficiency for a fast-growing bank, and why Nu Holdings already generates $3.2 billion in net income on $16 billion in revenue. Expect net income to increase faster than revenue as the business continues to expand.

We can look at this in another light. As Nu’s monthly average revenue has increased, its cost to serve has remained little changed during the past few years, freeing up more and more profit dollars to flow to the bottom line. Its monthly revenue per active customer is now $16, while its cost to serve is just $1, another example of the bank’s incredible efficiency.

If Nu Bank’s revenue doubles during the next five years to $32 billion, its net income can triple to about $10 billion. Compared to its market cap of $63 billion, that gives it a five-year forward price-to-earnings ratio (P/E) of just 6. This is cheap for a fast-growing bank, and it gives Nu Holdings multibagger potential for investors willing to hold for the long term.