Zimbabwe’s Lithium Pivot: Promises and Pitfalls of Mining

Zimbabwe’s Lithium Pivot: Promises and Pitfalls of Mining

By Julie Radomski, Tsitsi Musasike, Tinotenda Chidhawu, Hudson Mtegha and Earnest Rungano Chinyanga

Lithium has emerged as an indispensable resource powering the energy transition, given its central role in electric vehicle batteries and battery energy storage systems. For Zimbabwe, endowed with Africa’s largest lithium reserves, this presents a historic opportunity. The country accounted for nearly 10% of global lithium production in 2025.

The Zimbabwean government’s February 2026 ban on all raw mineral ore and lithium concentrate exports signals a more assertive push toward local beneficiation and local value capture. In principle, the measure strives to move Zimbabwe’s lithium sector beyond upstream extraction toward midstream processing and downstream industrial development. The policy also reshapes Zimbabwe’s engagement with foreign investors—particularly Chinese companies that currently dominate lithium mining operations and global refining capacity. Yet without a coherent national strategy or the infrastructure required to support refining and manufacturing, the ban may complicate investor engagement without guaranteeing greater domestic value addition.

In a new report on leveraging mineral extraction for Zimbabwe’s socio-economic development, translating its geological advantage into broad-based, sustainable development is an urgent governance challenge.

The Promise of a Lithium Boom

Mining has long been central to Zimbabwe’s economy, accounting for 14 percent of GDP, 75 percent of export earnings and 20 percent of government revenues in 2024, according to the World Bank Group. Lithium alone contributed $209 million to mining exports in 2023, with production increasing from just over 20,000 metric tons in 2020 to more than 826,000 metric tons in 2023. The government’s ambitious Vision 2030 relies in part on the mining sector as a pillar of growth to propel Zimbabwe into becoming an upper-middle income country.

This dramatic growth has attracted substantial foreign investment since 2021, particularly from China. Chinese companies are responsible for approximately 60 percent of the world’s lithium refining capacity and 70 percent of lithium-ion battery production. To sustain these industries, China imports much of the lithium it extracts from Australia, Chile, Argentina, and increasingly, Zimbabwe. Across all currently operating lithium mines in Zimbabwe, there is significant Chinese involvement in all six. Chinese private companies have invested over one billion dollars in acquiring and developing lithium projects in Zimbabwe since 2021. Several of these companies have also invested in processing plants to produce lithium sulphate in Zimbabwe, including Huayou Cobalt at the Arcadia mine, Yahua Group at Kamativi and Sinomine at Bikita.

Figure 1: Map of Lithium Mining Sites in Zimbabwe

Despite the boom in investment in the lithium sector, Zimbabwe lacks a standalone mining policy or transition mineral strategy to guide the sector’s growth, manage environmental and social risks and map a course towards midstream, downstream or sidestream development. Instead, Zimbabwe’s mining sector remains governed by the 1961 Mines and Minerals Act, a colonial-era legislation ill-suited to modern extractive governance. Although a revised Mines and Minerals Bill was gazetted in 2025, it has yet to be enacted, and moreover, is not crafted in line with a robust strategic policy framework.

The African Union’s Africa Mining Vision (AMV) outlines four interconnected streams in mineral development: upstream (extraction), midstream (processing and refining), downstream (manufacturing) and sidestream (infrastructure, skills and technology development). Currently, Zimbabwe remains overwhelmingly focused on upstream activities, with limited movement toward capturing value at subsequent stages.

The government’s 2022 ban on raw lithium exports and reported ban on lithium concentrate exports beginning in 2027 intended to promote local beneficiation, but in practice, loopholes have allowed raw ore to continue flowing abroad. The government subsequently announced the February 2026 immediate ban on export of all raw minerals and lithium concentrates after investigations revealed stockpiles of mineral ores at the Port of Beira in Mozambique.

The sudden announcement of the lithium concentrate export ban underscores the fragmented nature of mineral governance in Zimbabwe: ambitious policy signals are not yet matched by an integrated strategy for industrial development, infrastructure expansion or regulatory enforcement.

Instead, recent investment in the lithium sector has catalyzed production, but also raised environmental and social concerns. The report uses a mixed-method investigation—combining surveys of 230 respondents across all six mining sites with key stakeholder interviews—which paints a troubling picture of the lithium sector’s impact on development in practice.

Communities at the Frontline

While residents in the communities surrounding lithium mining sites acknowledge some employment and other economic opportunities, when asked about socio-economic development in their areas, 40 percent rated it as “poor,” 50 percent as “fair” and a mere 19 out of 230 respondents across all sites rated it positively (Figure 2). Employment opportunities for locals are concentrated in low-skilled and unskilled roles, with white-collar and technical opportunities remaining limited.

Figure 2: Responses on Whether the Area is Moving Forward in Terms of Socioeconomic Development

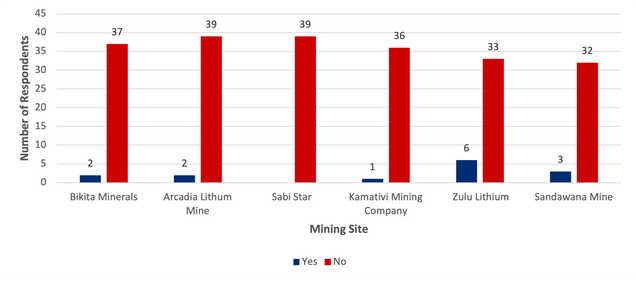

Further, survey results reveal profound dissatisfaction regarding local engagement. An overwhelming 94 percent of respondents reported feeling their input and feedback was not valued by mining companies, also identifying a lack of meaningful consultation or even communication on the part of these mines. This is a serious concern for communities across all mining sites, regardless of the ownership structure or nationality of the companies involved (see Figure 3).

Figure 3: Responses on Whether Community Input is Valued

Government officials and company representatives emphasize that Environmental and Social Impact Assessments are mandatory and are overseen by the Environmental Management Agency. However, civil society and survey data attest that implementation and ongoing monitoring is lacking. Air pollution (identified by 84% of respondents) and noise pollution (72%) top the list of environmental concerns, according to the results shown in Figure 4. In areas like Sandawana and Kamativi, land use change and appropriation emerged as significant issues (42% overall), with communities also reporting inadequate compensation and consultation during displacement or resettlement processes.

Figure 4: Environmental Concerns Regarding the Mining Sites

In light of the lithium concentrate export ban, these results highlight that expanding technical training and engagement with communities located near extraction sites is critical to ensure that local populations can access opportunities beyond low-skilled mining jobs as the sector evolves.

Infrastructure Bottlenecks

Infrastructure presents another critical challenge for both local communities and the mining industry. Companies are not legally obligated to provide public infrastructure, yet lithium mining’s expansion is itself contributing to straining Zimbabwe’s already fragile infrastructure. Roads serving the mining sites and surrounding areas, originally built for passenger traffic, are deteriorating under the weight of trucks transporting heavy ore. The research team documented a bus stuck on damaged roads and excessive dust pollution on gravel routes to and/or near mines as shown in Figure 5. The country’s rail network is now largely defunct, forcing this unsustainable reliance on road transport.

Figure 5: Bus stuck on the road near Sandawana Mine

Beyond transport, energy and water infrastructure face similar pressures. While some companies have invested in last-mile transmission lines and substations (Bikita, Arcadia) or even coal-fired power plants (Sabi Star), these investments remain fragmented and primarily serve individual mining operations. If Zimbabwe intends to process lithium domestically, the mining policy raises urgent questions about whether the country’s infrastructure—particularly electricity, water and transport systems—can support energy-intensive refining operations.

The report calls for an integrated infrastructure development strategy, arguing that the Mutapa Investment Fund (MIF)—Zimbabwe’s sovereign wealth fund—could play a catalytic role as a co-financier in public-private partnerships (PPPs) for infrastructure. Established in 2015 and restructured in 2023, the MIF receives at least 25 percent of mining royalties and dividends from state-owned enterprises. By leveraging resource revenues and mining companies’ offtake guarantees, MIF could support rail rehabilitation, renewable energy and water management systems that benefit both industry and communities.

To achieve this, transparency, strong governance and political will are critical. Lessons from Norway’s sovereign wealth fund and emerging African examples like Ethiopia’s Industrial Holdings fund suggest that clear fiscal rules and independent oversight are essential for credibility and effectiveness.

Building an Inclusive Lithium Economy

The February 2026 export ban marks an inflection point for Zimbabwe’s lithium mining sector. If accompanied by coherent industrial policy, infrastructure investment and stronger regulatory oversight, it could push the country toward capturing greater value from its mineral wealth. If not, it risks creating uncertainty for investors while doing little to change the underlying dynamics of extractive development.

Realizing the sector’s developmental potential will require:

- Strengthening policy coherence: Strengthen the policy framework for the mining sector (including lithium) through a clear, transparent, coordinated and inclusive consultation process.

- Enhancing inclusion: Institutionalizing benefit-sharing and participatory planning mechanisms rather than relying on ad hoc corporate social responsibility (CSR).

- Improving governance capacity: Strengthen government agencies’ policy making, implementation, monitoring and enforcement processes through capacity building that emphasizes transparency and accountability in relation to environmental and social governance.

- Increasing the role of the knowledge community: Strengthen the role of academia, think tanks, consultancies and civil society experts across training, research, policy advocacy, formulation and oversight, while investing in research and curriculum development to drive innovation.

- Investing in infrastructure: Strengthen the capacity of the MIF to drive initiatives around investment in infrastructure such as transportation, energy, and water management.

- Expanding partnerships: Develop and diversify international partnerships that advance both parties’ economic and development priorities.

If these steps are implemented, Zimbabwe could not only solidify its position as Africa’s leading lithium producer but also become a blueprint for transformation. The report findings indicate that course correction is urgently needed to avoid perpetuating extractive patterns of historical resource booms. However, this window of opportunity could disappear overnight given the rapid pace of change in technological advancement, and must be acted upon urgently.

*

Credit: Source link

Comments are closed.